| |

principal of the fund. For example, loan funds and

working capital funds. The capital amount of a fund

may be in the form of cash, inventory receivables, or

other assets.

Defense Business Operating Fund

Of the several funds, the one that you will be most

concerned with is the Defense Business Operating Fund

(DBOF). It is not practical for each activity of the Navy

to purchase all of its requirements directly from

commercial suppliers using its operating money. It is

for this reason that the DBOF exists. It provides the

necessary capital to finance the purchase and

maintenance of stocks of common supply items

required by the Navy. Basic capital for the DBOF is

made available from Congress. The total value of the

DBOF is reviewed annually by Congress and adjusted

to meet current requirements. Within the Navy, the

Commander, Naval Supply Systems Command is the

administrator of the DBOF.

DBOF CHARGES—The Defense Business

Operating Fund is charged with the following:

Expenditures for the purchase or manufacture of

stores, supplies, equipment, and services which

are to be taken up in the Navy Stock Account

(NSA).

Appropriation adjustments lodged against the

fund for sale of materials from a stores account

to the Navy Stock Account. They are used for

return “with charge” of material previously

charged to an end-use functional account.

Navy Stock Account losses by accounting, price

adjustment, appraisal, inventory, sale, and

survey, which are not properly charged to an

appropriation.

Donations of surplus NSA material for public

health and educational purposes, including

research.

Authorized charges for repair of NSA material

in store.

Issues from the NSA of clothing items for health

and comfort, when not chargeable to another

appropriation.

Payment of claims approved by the General

Accounting Office (GAO).

DBOF CREDIT—The DefenseBusiness Operating

Fund is credited with the following:

Issues from the NSA charged to an appropriation

or fund.

Cash sales from the NSA (including sales to

other government departments and foreign

governments),

Sales from the NSA to other stores accounts.

Collections from carriers for NSA material lost

or damaged in transit.

NSA gains by accounting, price adjustment,

appraisal, inventory, sale, and survey which are

not properly creditable to an appropriation.

Reimbursements from the Defense Logistics

Agency for the pro rata share of proceeds from

sale of surplus, scrap, and salvage material

expended from the NSA.

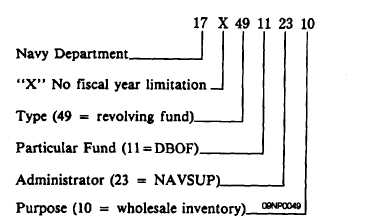

DBOF SYMBOLS—Symbols used in the elements

that make up the DBOF serve the same purpose as those

for appropriations. They identify charges and credits

made against the DBOF. The symbols used in the

construction of the DBOF consist of eleven digits. The

first seven digits designate the department responsible

for administering the fund; an indicator of fiscal year

limitation, the type, and the particular fund. The other

four digits compose the subhead. It identifies the

command or bureau within the Navy responsible for

administrating this element of the fund and the purpose

for which it is to be used. The meaning of each digit or

combination of digits is shown in figure 9-4.

DBOF Use—DBOF fulfills its role as a revolving

fund by purchasing designated supplies from

commercial sources, Defense Logistics Agency, the

General Services Administration, and the Departments

of the Army and Air Force, and then selling them.

These supplies maybe sold to a specific appropriation

Figure 9-4.-Example of a Defense Business Operating Fund

symbol.

9-4

|