| |

1721804, the 17 refers to the Department of Navy,

the 2 refers to the fiscal year 1992, and the 1804

refers to the type of appropriation—O&MN in

this case.

Subhead Symbol

The four-character subhead symbol for the

O&MN appropriation identifies the major

claimant and major program of the FYDP. The

first two characters are the last two characters of

the major claimant’s UIC. The third character is

the major program of the FYDP or budget

activity. The fourth character is a zero at the

major claimant (fleet) level. For example, in

subhead symbol (17xxxxx.)6020, the 60 refers to

the major claimant’s last two characters of the

UIC (COMNAVLANTFLT), the 2 refers to the

number of FYDP (General-Purpose Forces), and

the 0 refers to fleet level.

Expense Limitation

An expense limitation will cite the same

subhead from which issued except that the fourth

character of the four-character symbol will be a

significant alphabetic or numeric character

assigned by the major claimant to identify the

expense limitation holder. Expense limitations

are issued on a Resource Authorization, NAV-

COMPT Form 2168-1. In the subhead symbol

602E, the first three characters mean the same as

explained in the Subhead Symbol section just

covered; however, the E in the fourth character

identifies the expense limitation holder, or

Commander, Naval Air Force, U.S. Atlantic Fleet

in this case.

Operating Budget

Operating budgets are issued from expense

limitations to responsibility centers on a resource

authorization and are designated by the UIC

of the responsibility center. Fleet and type

commanders issue operating budgets to them-

selves for centrally managed programs and for

their subordinate cost centers (units). When more

than one operating budget is issued to a

responsibility center from the same expense

limitation, the operating budgets are distinguished

by appending a one-character alphabetic or

numeric suffix (for example, 57014R) to the

operating budget number. To simplify the

identification of the specific operating budget

chargeable on each requisition or other financial

document, two-character fund codes are estab-

lished by the Office of the Comptroller of the

Navy. Fund codes used by the Operating Forces

are contained in appendix II of NAVSO P-3013-2.

Operating Target

Operating budget holders will establish

OPTARs as required to separately identify costs

and to permit command and management to

follow the same channels. OPTARs will not be

issued for other operating targets, but will be

issued direct from an operating budget by the

operating budget holder down through one or

more levels in the command structure. OPTARs

are not designated with a distinguishing

identification number. The combination of the

applicable fiscal year service designator (R for

Pacific Fleet units and V for Atlantic Fleet units),

UIC of the OPTAR holder, and the fund code

applicable to the operating budget provides the

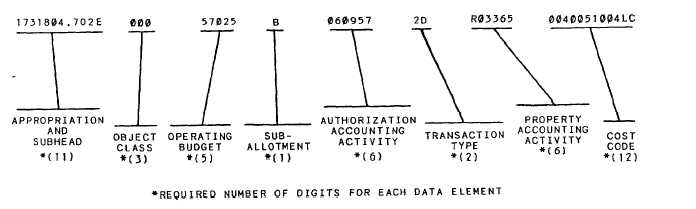

complete accounting classification. (See fig. 3-2.)

Reimbursable Orders

A reimbursable order is a request for work or

services to be performed on a reimbursable basis

Figure 3-2.—Format of accounting data.

3-3

|