| |

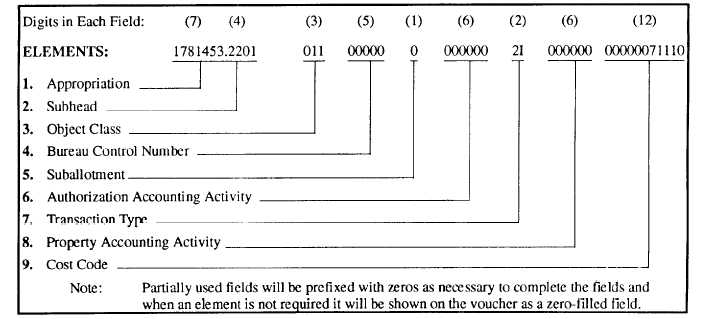

example of an accounting classification code that

contains the maximum number of elements is shown in

figure 2-2. Figure 2-2 also illustrates the order in which

the accounting data should be entered on the required

documents. You should follow the order shown in

figure 2-2, regardless of any preprinted instructions on

your document to the contrary. In the following

sections, we will explain the significance of each of

these elements and the order in which they should be

used.

We will also examine the position and

significance of the alphanumeric characters in each

element. While reading this information, remember to

refer to the example in figure 2-2. We will discuss these

elements and their characters in the order of their

numerical and sequential presentation in this figure.

APPROPRIATION OR FUND

In every accounting classification code, the first

element represents the appropriation or fund. (Refer to

number 1 on the left side of figure 2-2. This represents

the first element in the accounting classification code

used as the example.) The appropriation or fund, of

course, indicates the legal source of each transaction.

In most cases, the appropriation code will consist of

only seven alphanumeric characters. It may, however,

contain up to nine characters, depending on the

reporting requirements.

The first two digits in our example are 1 and 7, or

17, which represent the Department of the Navy. The

third digit, 8, is the last digit of the fiscal year for that

in the third position instead of a number, then the

appropriation is a continuing appropriation. If the letter

M is used in the third position, then the appropriation is

a successor appropriation.

The next four digits (1453) indicate the type of

appropriation. In the case of a fund, these four digits

would indicate the type of appropriation and the

particular type of fund used within that appropriation.

SUBHEAD

The second element of the accounting code

(indicated as number 2 on the left side of the figure) is

the subhead. This element identities the charges (or

credits) to the appropriation or fund (indicated in

element 1) for that particular transaction. The subhead

consists of four characters. The first two characters

identify the administering offices. The last two

characters identify the purpose of the subhead. For

example, the subhead 2201 in figure 2-2 identifies the

administering office, 22, as the Bureau of Naval

Personnel (BUPERS) and the purpose, 01, as pay and

allowances of officer personnel.

OBJECT CLASS

The object class is the third element in the

accounting classification code. (Refer to number 3 in

figure 2-2.) It consists of three digits. The object class

designates the nature of the services, articles, or other

items involved, as distinguished from the purpose for

particular annual appropriation. If the letter X is used

which obligations were incurred.

Figure 2-2.-The accounting classification code.

2-4

|