| |

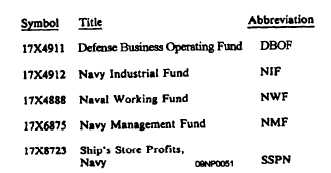

Figure 9-6.-Examples of various fund symbols.

ACCOUNTING FOR

APPROPRIATIONS

The receipt and expenditure of a matter of

public record that must be

accounted for and when necessary

justified. This is accomplished by the accounting

classification system. The purpose of the system

is to classify expenditures as to their type or

purpose, and to designate the activity responsible

for recording and maintaining official records of

these expenditures.

An explanation of elements that make up the

accounting classification system (commonly referred to

as line of accounting) is given in the following

paragraphs. Study the discussion of the system very

carefully. It will be your responsibility to use the proper

classification on procurement and expenditure

documents that you prepare. See figure 9-7. We have

previously discussed the appropriation and subhead we

will begin with the next element in the line of

accounting, the object class.

OBJECT CLASS

Object class codes are three characters long, and are

used only in OPTAR transactions which affect the

international balance of payments. These codes are

contained in NAVCOMPT Manual, Volume 2.

OPERATING BUDGET (BUREAU

CONTROL NUMBER)

The CNO has fiscal responsibility for the

appropriation 1751804 for operation and maintenance

of Navy forces. In discussing appropriations, you saw

how they may be apportioned. The responsibility for

administrating the appropriation is shown by subhead.

However, it is not possible for one office to efficiently

control all charges to this appropriation. It is allocated

to subordinate commands to administer.

For example, one of these commands is

CINCPACFLT. It is still impractical for the one office

to administer the appropriation to the hundreds of ships

under command. Portions of the appropriation then, are

granted to PACFLT TYCOMS (e.g., COMNAVSURF-

PAC, COMNAVAIRPAC, etc.) in the form of operating

budgets. Operating budgets are identified by an

operating budget number which is always the unit

identification code (UIC) of the activity receiving the

operating budget grant. For example, the operating

budget number for a grant to COMNAVSURFPAC

would be 53824.

SUBALLOTMENT/OPERATION

BUDGET SUFFIX

When a budget holder has two or more operating

budgets, then a suffix is used to identify the different

operating budgets.

For example, CINCPACFLT

receives two operating budgets. One for ship repair, the

other for fuel. Both under operating budget number

00070 and subhead 702A. To identify the separate

grants, CINCPACFLT assigns operating budget suffix

code R to identify charges for ship overhaul and

operating budget suffix code F to identify charges for

ship’s propulsion fuel.

Figure 9-7.-Format of accounting data..

9-7

|